David Stewart

- Advisor at Approov / Former CEO of Approov

30+ years experience in security products, embedded software tools, design services, design automation tools, chip design.

This is the second article in our 3 part review of trends in the Mobility market. If you missed the first part, you can find it here.

Electric vehicles (EVs), with a mere 1.7% market share in 2019, are still at least a few years away from going mass market. This segment is expected to hit mass market adoption by 2025 and then build up to a share of about half of all new car sales by 2040.

After all the talk about deploying fully autonomous vehicles by the end of this decade, “the idea of full autonomy went a bit behind the curtain in 2019 and ADAS took more of center stage.” In Q2 2019, cars with ADAS (Advanced Driver Assistance System) features – corresponding to Level 2 autonomy on the SAE standard defining six levels of autonomy – accounted for just 10% and 8%, respectively, of all new cars sold in the US and Europe.

On-demand mobility concepts, such as ride-hailing, have the comparative scale and the potential to plug gaps in modern consumers’ journeys. However, they are still operated as a discrete service that, as we argued in our previous article of The Rise of On-Demand Mobility, neither offers practical alternatives to car ownership nor addresses issues related to congestion and emissions.

Even as the buzz around mobility-as-a-service models continues to grow, there is very little evidence that they have had any significant impact on the current operating dynamics of traditional auto OEM business models. For instance, there has been no radical revision in the short-term challenges facing the traditional automotive value-chain; issues, such as geopolitical and macroeconomic risks, new emission standards and penalties, competitive market dynamics, etc. are all still in need of a solution.

However, the mid- to long-term challenges have now been completely rewritten to include new mobility issues such as monetizing the shift from ownership to Mobility-as-a-Service and the consequent need for investment in new technologies.

The strategic challenge for auto OEMs, then, is to continue focusing on their conventional operations even amid dire predictions that revenue and profits from manufacturing and selling vehicles will yield increasingly lower returns leading up to 2030. Over the same period, mobility-as-a-service will grow exponentially, with the potential to generate nearly $1.2 trillion in revenues and $220 billion in profits. So, auto OEMs will also need to invest to create and consolidate their positions in an emerging market defined by the convergent trends of Mobility-as-a-Service, EVs and AVs.

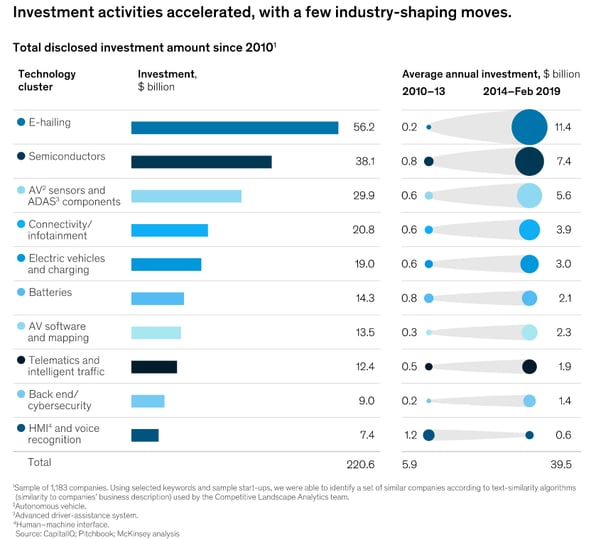

Investments into the mobility space have been growing. According to a McKinsey analysis, new mobility startups have attracted nearly $220 billion in investments since 2010, with more than half of that coming in the form of $1 billion plus transactions. These investments were distributed across ten technology clusters, with e-hailing, semiconductors, and AV sensors/ADAS components making the top three investment destinations.

SOURCE: McKinsey

However, over 90% of these investments have come from investors, venture capitalists and private-equity funds from outside the automotive business.

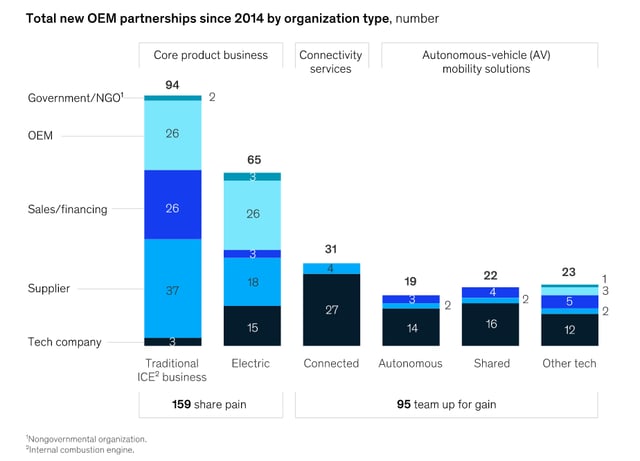

Now, not many auto OEMs may be in a position to spare the estimated sum of $70 billion, per OEM, required to build a strong position across shared, connected, electrified and autonomous mobility in the midst of their struggle to balance innovation with survival. So, almost all of them have turned to a strategy that they have thus far used with limited scope but to great success in their traditional business – cooperation.

SOURCE: McKinsey

For OEMs, building partnerships in the shared mobility space is as much about sharing costs as it is about sharing the risks associated with developing, testing and deploying innovative new technologies. Today, there are numerous examples of partnerships between OEMs, suppliers, technology companies, and mobility service providers, etc. Here’s just an illustrative sample of how the industry is coming together to address new mobility opportunities.

And the list goes on as OEMs partner with self-driving technology companies, chip manufacturers, energy solution providers, ride-sharing services, etc., to develop the right mobility solutions. Over the long term, McKinsey predicts that these collaborations and partnerships will help evolve conventional auto value chains into mobility ecosystems.

From the consumers’ perspective, these mobility ecosystems will deliver a truly end-to-end, service-based transport model. This multimodal MaaS aggregation model integrates all mobility solutions, including public, private and on-demand, into one platform that allows consumers to plan, book and pay for different types of transport with a single interface.

A Finnish startup called MaaS Global, the world's first Mobility-as-a-Service operator, has been offering just such a service since 2017 through a mobile app called Whim. Using the app, city travelers can plan their routes combining multiple modes of transport, including trains, buses, taxis, rental cars and bikes, and book and pay for the journey through a unified interface.

CASE (Connected, Autonomous, Shared, Electric) technologies represent the inevitable future of mobility. For traditional OEMs, the challenge is to balance their current priorities of consolidating and improving operational and financial performance against the imperative to acquire and build the capabilities required to compete successfully in a MaaS world. As non-automotive investments and technologies flood the mobility market, traditional OEMs are turning to collaboration and partnerships with their industry counterparts and with CASE leaders to share the costs and risks of addressing this nascent market.

In the next and final part of this blog series, we will look the challenges of scaling up the deployment and use of the fundamental building block of MaaS, the connected car.

- Advisor at Approov / Former CEO of Approov

30+ years experience in security products, embedded software tools, design services, design automation tools, chip design.